About Course

PVC Patent Landscape Report

Scope

- Analysis of 49,233 patents from 2010–2025.

- Focus on technological advancements, market dynamics, and leading innovators in PVC.

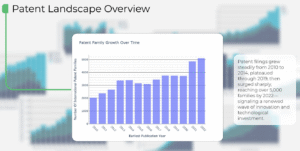

Key Findings

- Explosive Growth

- PVC patents grew eightfold between 2010 and 2025.

- Peak activity in 2022, indicating heightened innovation and commercial interest.

- Technology Focus

- Innovations center on advanced polymer chemistry, organic/inorganic compound compositions, and PVC recycling & environmental impact reduction.

- Geographic Dominance

- US and China account for 74% of PVC patents.

- China overtook the US in 2022 in annual filings.

- Market Potential

- Valued at USD 57.06B in 2022, forecasted to reach USD 78.92B by 2029.

- Driven by construction, packaging, and automotive sectors, with a CAGR of 4.5%.

Technology Trends

- Patent growth was steady from 2010–2014, plateaued until 2019, then surged sharply.

- Leading IPC subclasses: C08L and C08K – polymer compositions and additives (~16,000 patents combined).

- Dominant applicants include LG Chemical (700 patents, ~45% more than 3M), with strong competition in polymers, coatings, and electronics.

Strategic Recommendations

- Policy Makers – Promote sustainable technology development and targeted R&D investment.

- Investors – Prioritize firms with strong IP in high-growth PVC applications.

- Manufacturers – Adopt innovations for efficiency, scalability, and circular economy compliance.